The Core Structure of RWA: How Are Real-World Assets Tokenized?

The key to RWA isn't just "putting assets on-chain," but building a comprehensive structure that connects the real world with blockchain. This lesson will break down the core architecture of RWA to understand how real-world assets are tokenized step by step and integrated into the DeFi system.

I. Why Can’t Real-World Assets Go On-Chain Directly?

When many people first hear about RWA (Real World Assets), they often have an instinctive question: How can real-world assets possibly be put directly on the blockchain? To understand this, it’s necessary to clarify the basic attributes of blockchain.

Essentially, blockchain is a distributed ledger system that can record and verify digital information, such as:

- Digital asset balances

- Transaction records

- Smart contract states

- Token ownership

But most real-world assets are not purely digital information—they are physical assets or legal rights. For example:

- Real estate is a physical asset that requires ownership confirmation in a land registry system

- Bonds are legal debt relationships

- Gold is usually stored physically in vaults

- Corporate loans are legally binding contracts

Therefore, from a technical perspective:

- The blockchain cannot “store a house”

- The blockchain cannot “hold a batch of gold”

- The blockchain cannot “possess a loan contract”

The existence of these assets relies on real-world legal systems, custodians, and asset registration systems. This means the core of RWA is not directly transferring real-world assets onto the blockchain, but using a bridging mechanism to map the rights of real-world assets onto the blockchain.

This process can typically be represented by a simple structure: Real-world asset → Legal structure → On-chain token

In this structure:

- The real-world asset still exists in the physical world

- The legal structure is responsible for confirming asset rights

- The blockchain records the digitized expression of asset rights

This mechanism is commonly referred to as the RWA Tokenization Framework.

It forms the core connection between real-world assets and the blockchain.

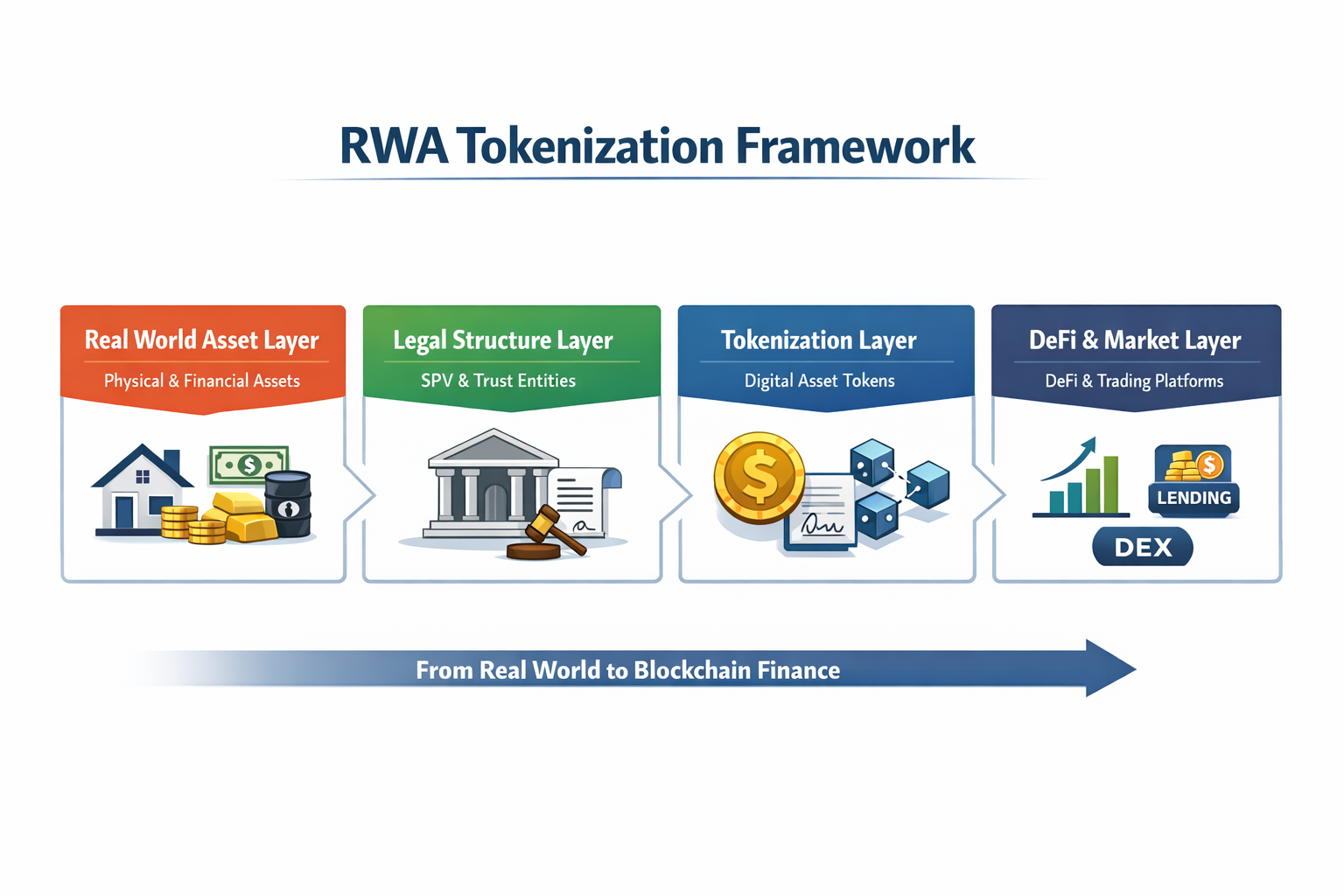

II. The Four-Layer Structure of RWA

From an overall architecture perspective, a complete RWA project usually consists of four core layers. These four layers together form the foundational structure for integrating real-world assets into the blockchain system.

| Level | Function |

|---|---|

| Asset Layer | Real-world assets |

| Legal Layer | Asset custody and legal structure |

| Token Layer | Asset tokens on the blockchain |

| Application Layer | DeFi and trading markets |

Real-World Assets (RWA) Framework

These four layers can be understood as a step-by-step mapping process from the real world to blockchain finance. Real-world assets first undergo rights structure design at the legal layer, then are tokenized and enter the blockchain network, and finally are utilized in DeFi or trading markets.

Layer One: Asset Layer (Real World Asset)

The starting point of the RWA system is the asset itself in the real world. Not all assets are suitable for tokenization. Generally, assets appropriate for RWA need to meet several criteria:

- Relatively stable value

- Clear income structure

- Well-defined legal ownership

- Auditable

Currently, the most common types of RWA assets in the market fall into three main categories.

1. Financial Assets

This is currently the largest category by market size in RWA, such as:

- Treasuries

- Corporate bonds

- Private credit

- Accounts receivable

These assets inherently have stable cash flows, making them very suitable for tokenization.

2. Physical Assets

The second category consists of tangible assets in the real world, such as:

- Real estate

- Gold

- Commodities

These assets usually have high value but low liquidity. Tokenization allows them to be divided into smaller investment shares.

3. Yield-Generating Assets

The third category includes assets capable of generating ongoing cash flow, such as:

- Real estate rental income

- Corporate loan interest

- Infrastructure returns

The income from these assets can be distributed via blockchain, creating new investment products. Currently, the fastest-growing RWA asset class is Treasuries. The reasons are straightforward:

- Stable returns

- Lower risk

- Huge market size

- Transparent pricing

Therefore, more and more DeFi projects are trying to bring Treasury yields on-chain.

Layer Two: Legal Structure (Legal Wrapper)

Within the RWA system, the legal structure is the most critical layer. Blockchain can only record digital information, while ownership of real-world assets must be confirmed through legal systems. As a result, most RWA projects establish a legal entity to hold assets. The most common structure is an SPV (Special Purpose Vehicle).

An SPV is a specially established legal entity whose main functions include:

- Holding real-world assets

- Isolating asset risk

- Managing investor rights

- Supporting on-chain token issuance

For example, a typical RWA project might operate as follows:

- Establish an SPV company

- The SPV uses funds to purchase $100 million in Treasuries

- The SPV issues corresponding tokens on the blockchain

In this structure: Token holders do not directly own the Treasuries but instead hold asset rights represented by the SPV. This structure is actually very common in traditional finance, such as:

- Asset-backed securities (ABS)

- Real Estate Investment Trusts (REITs)

Essentially, RWA brings traditional asset securitization structures onto the blockchain.

Layer Three: Tokenization Layer (Tokenization)

Once the real-world asset and legal structure are established, the next step is asset tokenization. The core of tokenization is converting asset rights into tokens on the blockchain.

These tokens can represent: asset ownership, income rights, or debt claims.

Suppose an RWA project holds $10 million in Treasuries. The project team can issue 10 million tokens, with each token representing $1 worth of Treasuries.

Investors can receive corresponding asset returns by purchasing tokens. Blockchain offers several key advantages at this stage:

- Transparency: All token issuance and transactions can be publicly verified on-chain.

- Programmability: Smart contracts can automate income distribution.

- Global liquidity: Investors worldwide can participate in asset trading.

Layer Four: On-chain Application Layer (DeFi)

After RWA tokens are issued, they can enter the broader DeFi ecosystem. Common application scenarios include the following categories.

1. On-chain Trading

RWA tokens can circulate in trading markets such as:

- Decentralized exchanges (DEX)

- Centralized exchanges (CEX)

Investors can buy and sell these tokens just like trading crypto assets.

2. Collateralized Lending

RWA tokens can also be used as collateral for lending activities, such as:

- Using RWA tokens as collateral to borrow stablecoins

- Participating in leveraged trading

This allows real-world assets to participate in on-chain financial activities.

3. Yield Products

RWA assets can also be combined with other DeFi assets, such as:

- Yield pools

- Structured products

- DeFi strategies

For example: Stablecoins + Treasury RWAs can form a relatively low-risk on-chain yield product.

Key Roles in the RWA Ecosystem

A complete RWA system typically involves multiple participants.

| Role | Duties |

|---|---|

| Asset Issuer | Provides real-world assets |

| SPV / Legal Structure | Holds assets |

| Custodian | Stores assets |

| Oracle | Provides asset data |

| Blockchain Protocol | Issues tokens |

| DeFi Platform | Provides application scenarios |

RWA: Real-World Asset Tokenization

RWA is essentially a hybrid financial system combining on-chain and off-chain elements. Blockchain is responsible for transactions and asset representation, while real-world institutions handle asset management and legal protection.

Why is the RWA structure so complex?

Many people find RWA structures complicated when they first learn about them, mainly because the traditional financial system itself is highly complex.

For example:

- Real Estate Investment Trusts (REITs)

- Asset-Backed Securities (ABS)

- Mortgage-Backed Securities (MBS)

These financial products inherently require legal structures, custodians, audit firms, and investment managers. RWA does not change these financial structures; it simply adds blockchain technology to the existing financial system.

Summary

The core of RWA is not just “asset tokenization,” but building a complete financial architecture that connects real-world assets with blockchain.

A full RWA system typically includes four key layers:

- Asset layer: real-world assets (sovereign bonds, real estate, etc.)

- Legal layer: SPV or trust structure

- Token layer: asset tokens on the blockchain

- Application layer: DeFi and trading markets

With this structure, real-world assets can:

- Be traded on blockchain networks

- Be used in the DeFi ecosystem

- Be accessible to global investors

This is why more and more institutions see RWA as a crucial bridge connecting traditional finance and the blockchain world.

Lesson 1:What is RWA? Understanding the Basic Concept of Real World Assets On-Chain

Lesson 2:How Does RWA Work? The Complete Process of Bringing Real-World Assets On-Chain

Lesson 3:The Core Structure of RWA: How Are Real-World Assets Tokenized?

Lesson 4:Main Types of RWA Assets: Which Real-World Assets Are Entering the Blockchain?

Lesson 5:Why Has RWA Suddenly Exploded? The Three Driving Forces

Related Courses

The Beginner's Guide to Blockchain-based Airdrops

Crypto Mining Equipment

Learn about web3 data and analytics

Identity in Crypto: Main Projects

Introduction to Masternode Tokens