A Decade of Regulation Finally Clarified: A Victory for Crypto-Native Logic

BTC, ETH, SOL, XRP, DOGE, SHIB.

For the first time, these names have appeared together in an SEC regulatory filing, each explicitly labeled: not securities.

On the evening of March 17, 2026, the SEC and CFTC jointly released a 68-page interpretive document, formally defining the securities status of crypto assets. This marks the first instance at the US federal level where a regulatory explanation specifically identifies individual tokens and assigns classification outcomes. The document also supersedes the SEC's 2019 "Investment Contract Analysis Framework," which had been the industry's main compliance reference.

The release of this document follows a clear timeline.

In January 2025, SEC Acting Chair Mark T. Uyeda established the Crypto Task Force to clarify the boundaries of securities law as applied to crypto assets. In July, the President's Working Group on Digital Asset Markets published a report recommending that the SEC and CFTC use their existing authority to provide regulatory clarity for the industry.

SEC Chair Paul S. Atkins subsequently launched Project Crypto, which was elevated to a joint SEC-CFTC initiative in January 2026. During this process, the Crypto Task Force received more than 300 public comment letters from issuers, investors, law firms, audit firms, and other stakeholders.

In short, this document represents a unified response from two federal regulatory agencies, delivered after more than a year of industry debate and policy coordination.

Five Categories—A Comprehensive Framework

In this document, the SEC divides crypto assets into five categories, using the four elements of the Howey Test as the core criteria.

The first category is Digital Commodities. This section has drawn the most attention, as the SEC provides a specific list of named assets: BTC, ETH, SOL, XRP, ADA, AVAX, DOGE, SHIB, LINK, DOT, LTC, BCH, HBAR, XLM, XTZ, and APT—a total of 16 tokens—are explicitly included in the main text. Footnotes also mention Algorand (ALGO) and LBRY Credits (LBC) as part of this category.

The SEC's rationale: These tokens derive their value from the programmatic operation of their underlying functional crypto systems, driven by supply and demand, not from expectations of profit based on the managerial efforts of others.

The second category is Digital Collectibles. CryptoPunks, Chromie Squiggles, WIF (dogwifhat), and VCOIN are specifically named. Meme coins are categorized here as well. The SEC finds their value is driven by "artistic, entertainment, social, or cultural significance," making them akin to physical collectibles and not securities.

The third category is Digital Tools. Examples include ENS domain names and CoinDesk's Microcosms NFT tickets. These assets provide functional utility—such as membership credentials, identity verification, or proof of ownership—and many are soulbound and non-transferable.

The fourth category is Stablecoins. Under the GENIUS Act, which has already been enacted, payment stablecoins issued by compliant issuers are explicitly excluded from the definition of securities. However, the SEC reserves jurisdiction over stablecoins that do not meet the Act’s requirements.

The fifth category is Digital Securities. This is the only category explicitly recognized as securities, but the SEC does not identify any specific tokens in this category within the document.

The boundaries between these five categories are not absolute. The SEC acknowledges the existence of hybrid assets that span multiple categories, as well as crypto assets that do not fit any category. The significance of this framework is that, for the first time, the question of "what is or isn't a security" has moved from courtroom debate to regulatory enforcement.

Four On-Chain Activities—Unified Characterization

Beyond token classification, the document makes another significant contribution by providing unified regulatory treatment for four core on-chain activities: mining, staking, wrapping, and airdrops.

Protocol mining is not considered a securities offering. Whether solo or in a pool, mining is a network maintenance function. Newly minted tokens are protocol-level programmatic rewards and do not create an investment contract relationship.

Protocol staking is not considered a securities offering. This determination covers four scenarios: solo staking, delegating to a third party while retaining key control, delegating to a custodian, and liquid staking. The SEC clarifies that staking rewards are generated by protocol-defined programmatic distribution, not by the managerial efforts of any team. For liquid staking tokens (LSTs) such as stETH, the SEC views them as "receipts" for underlying staked assets—not derivatives, and not securities.

Asset wrapping is not considered a securities offering. Wrapping BTC as WBTC for use on Ethereum is simply a technical interoperability process and does not alter the nature of the underlying asset.

Airdrops are not considered a securities offering. As long as recipients do not provide funds, goods, or services as consideration, the free distribution of tokens does not satisfy the "investment of money" requirement under the Howey Test.

These determinations have a direct impact on the industry: core DeFi protocol mechanisms—staking, wrapping, and airdrops—are now outside the reach of securities law. For the past three years, every project offering staking services or conducting airdrops has faced uncertainty. Now, there is a unified answer from federal regulators.

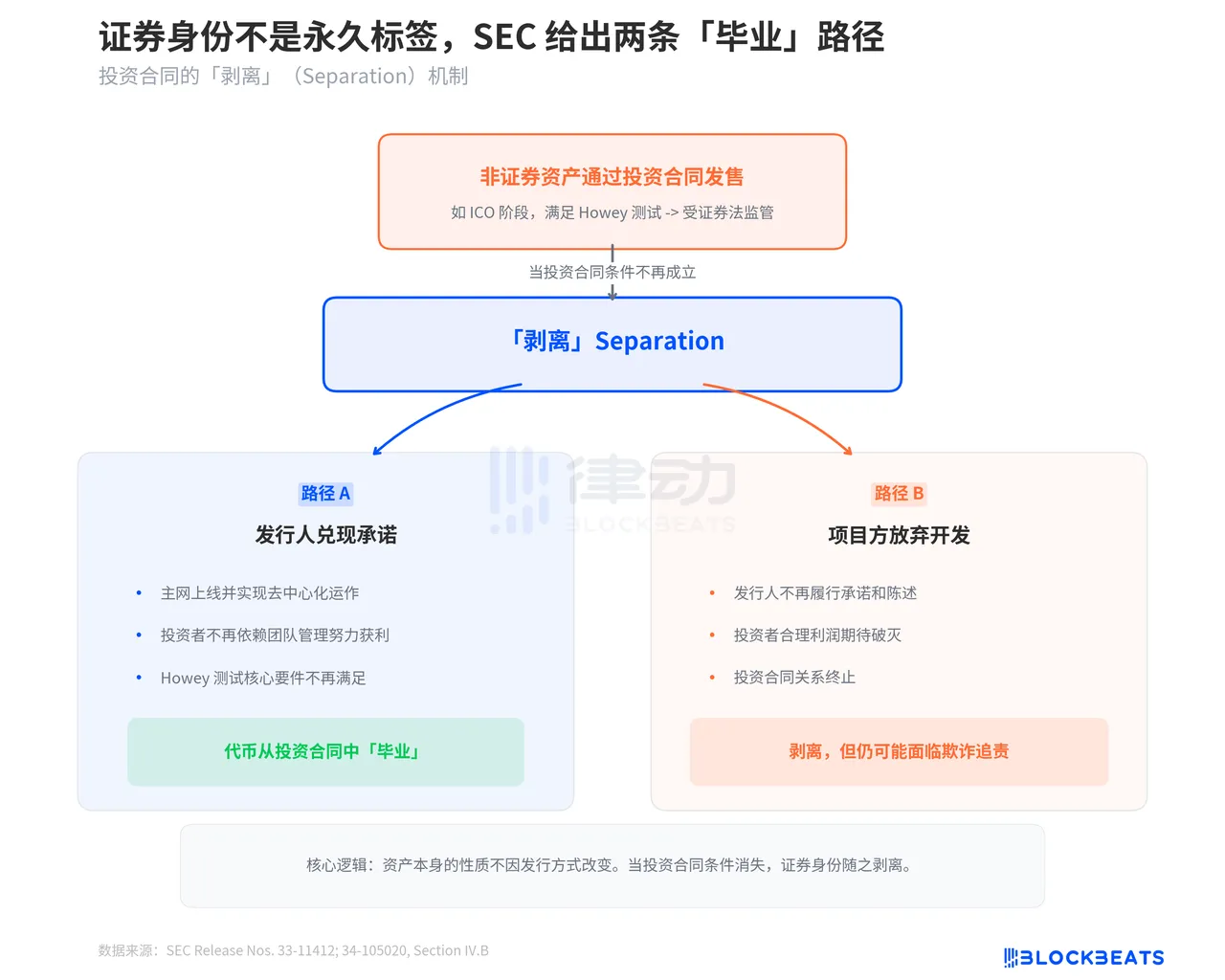

Securities Status Is Not Permanent

One of the most important sections of this document is the SEC's explanation of the Separation mechanism. The document makes clear that a crypto asset that is not inherently a security can fall under securities regulation if issued via an investment contract. However, once the investment contract conditions are no longer met, the asset can "separate" from its securities status.

The SEC outlines two separation scenarios. First, when the issuer fulfills its commitments. For example, a project promises during its ICO to develop a decentralized network; once the network launches and operates in a decentralized manner, investors no longer rely on the issuer's managerial efforts for profit. The core elements of the Howey Test are no longer satisfied, and the token "graduates" from its investment contract status.

The second scenario is more nuanced: the project team abandons the project. If the issuer no longer fulfills promises or statements made under the investment contract, investors' reasonable expectation of profit from "the efforts of others" disappears, ending the investment contract relationship. However, the SEC emphasizes that this does not absolve issuers of liability—they may still face fraud charges.

The true significance of the Separation mechanism is that it provides a compliant path for crypto projects. The process from ICO to mainnet launch to full decentralization is no longer a legal gray area, but a regulatory pathway with a clear endpoint. Once completed, the project exits the regulatory tunnel.

Sixty-eight pages. Nine chapters. Eighteen named tokens, six characterized on-chain activities, two graduation pathways. The SEC spent over a year collecting more than 300 comment letters, and ultimately, in partnership with the CFTC, delivered this framework. It is not perfect—stablecoin boundaries remain unclear, no specific examples are provided under "Digital Securities," and criteria for hybrid assets are still open for interpretation.

But for an agency once criticized for "regulation by enforcement," this document achieves at least one thing: it puts the rules in writing, not just in court filings.

Statement:

-

This article is reprinted from [BlockBeats]. Copyright belongs to the original author [BlockBeats]. If you have any objections to this reprint, please contact the Gate Learn team, who will handle your concerns in accordance with relevant procedures.

-

Disclaimer: The views and opinions expressed in this article are solely those of the author and do not constitute investment advice.

-

Other language versions of this article are translated by the Gate Learn team. Unless Gate is cited, reproduction, distribution, or plagiarism of the translated article is prohibited.

Share

Content

Related Articles

The Future of Cross-Chain Bridges: Full-Chain Interoperability Becomes Inevitable, Liquidity Bridges Will Decline

Solana Need L2s And Appchains?

Sui: How are users leveraging its speed, security, & scalability?

Navigating the Zero Knowledge Landscape

What is Tronscan and How Can You Use it in 2025?